How Stablecoins Are Becoming the Backbone of Digital Finance

Key Takeaways:

- Core Value: Stablecoins combine price stability with blockchain speed, enabling reliable digital payments and settlements.

- Comprehensive Services: They support payments, treasury management, remittances, DeFi, and Web3 applications.

- Business Benefits: Stablecoins reduce costs, speed up transactions, and enable seamless global payments for businesses.

- Industry Use Cases: Used across fintech, enterprise finance, global trade, remittances, DeFi, and Web3 ecosystems.

- Future Trends: Stablecoins will become embedded in global financial infrastructure with stronger regulation and interoperability.

Why Stablecoins are Gaining Momentum in Modern Finance?

Stablecoins are blockchain-based digital currencies pegged to stable assets like fiat currencies, enabling fast, low-cost, and reliable global transactions.

Money is moving very differently now than it did 10 years ago. Markets are global, payments are faster, and more and more financial activity is taking place online. But even with all this progress, traditional financial institutions are still hindered by limited access, high fees and slow settlement. This is exactly where stablecoins come into play.

People searching for how stablecoins are used in finance often want to understand why these digital assets are popping up everywhere from decentralized platforms to enterprise finance to international payments. Stablecoins are no longer a niche cryptocurrency idea. They are beginning to serve as a bridge between the digital economy and traditional financial systems.

Their rise is not built on hype and conjecture. It is driven by utility. Stablecoins are already delivering real value and proving more efficient than many outdated financial systems.

Many enterprises are combining stablecoins with blockchain development services to build customized financial systems that reduce operational overhead.

What Are Stablecoins in Digital Finance?

Stablecoins are digital currencies designed to maintain a stable value. Some are backed by reserves or baskets of assets, but most are pegged to fiat currencies such as the US dollar. The defining characteristic is stability. By the end of 2025, the global stablecoin market capitalization crossed $300 billion, reflecting rapid institutional and consumer adoption.

Digital finance requires stability. Businesses cannot operate on highly volatile assets. Consumers can’t rely on money that bounces so much. Stablecoins are built on blockchain networks and have the stability of traditional money.

Stablecoins are particularly powerful as they can be easily integrated into today’s financial processes. They can be paid without waiting for middlemen, sent instantaneously, held digitally without a bank account, and built into applications.

Stablecoins are thus no longer considered experimental cryptocurrency assets. They are increasingly viewed as a useful digital currency.

If you want a deeper understanding of how stablecoins function within the crypto economy, you can explore this detailed guide on stablecoins and their working mechanism.

Explore how stablecoin-powered systems can improve your payment infrastructure and financial operations.

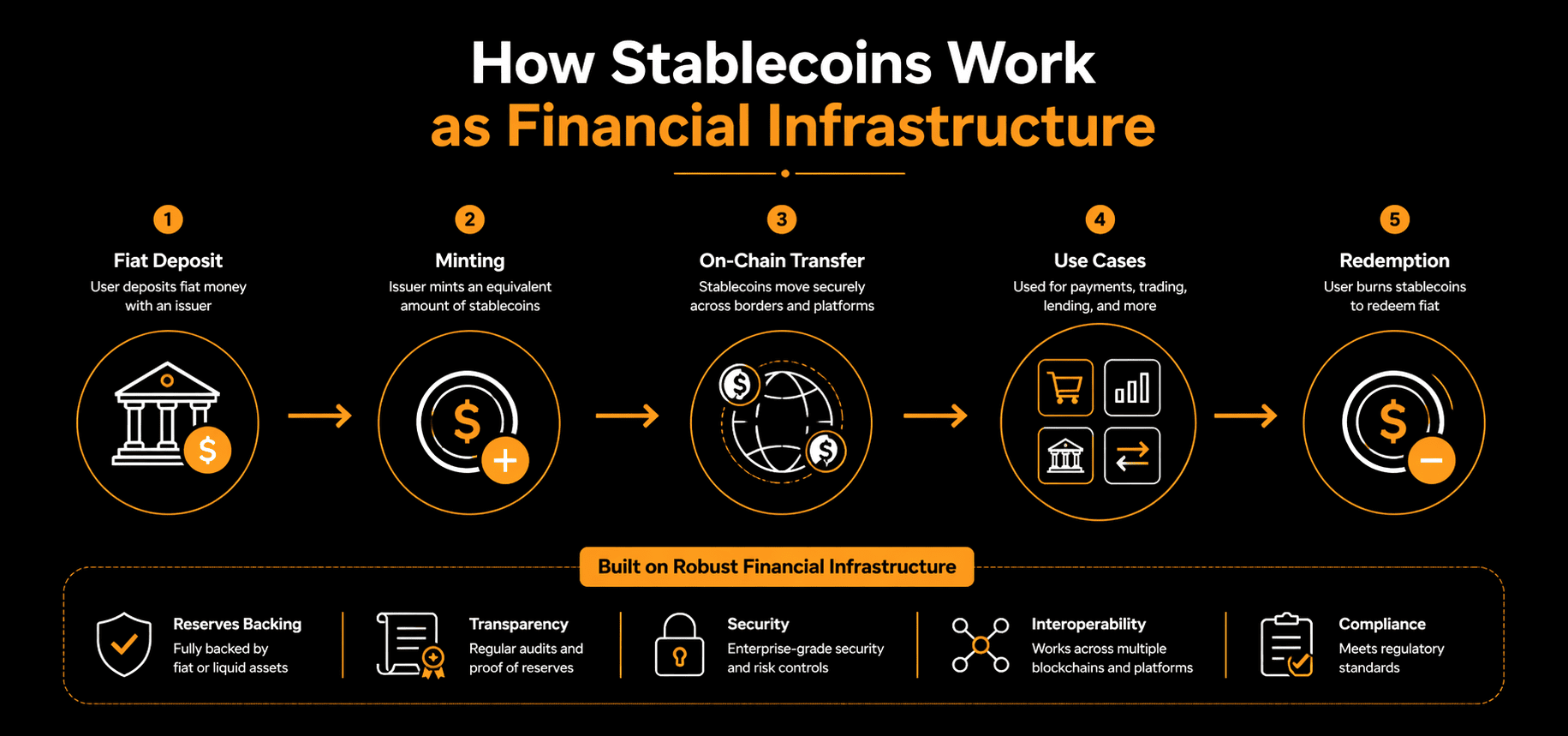

How Stablecoins Work as Financial Infrastructure?

To understand why stablecoins matter, it helps to think of them as infrastructure rather than products.

When fiat money is deposited with an issuer, an equivalent amount of stablecoins is minted on a blockchain. These tokens can then move freely across borders, networks, and platforms. Users can redeem their tokens at any time by burning them in exchange for the underlying fiat currency. This system is often built on advanced blockchain architectures, such as cross-chain smart contracts, enabling seamless asset movement across multiple networks.

This system enables continuous, 24/7 financial operations. There are no geographical limits, no settlement windows, no banking hours. That is why many experts refer to stablecoins as payment infrastructure, and not only as a digital currency. According to Forbes, in 2025, stablecoins processed over $33 trillion in on-chain transactions, confirming their role as global settlement infrastructure.

Stablecoins enable parties to settle directly, instead of having to go through the many intermediaries of traditional systems. This opens up new kinds of financial models and also changes the way money flows through the Internet.

Why are Stablecoins Becoming the Backbone of Digital Finance?

The rise of stablecoins is a direct response to the inefficiencies of the traditional banking system.

Transfers across borders may take days. Fees are typically costly and difficult to locate. Millions of people still lack access to banking around the world. Stablecoins solve each of these problems in a simple, but effective way. A 2026 fintech survey shows that 64% of enterprises already use or plan to adopt stablecoins for payments and treasury operations.

Another important benefit is how stablecoins reduce transaction costs. Stablecoins are a lot cheaper and faster than traditional payment rails, removing layers of middlemen and automating settlement.

Another factor influencing adoption is accessibility. Anyone with an Internet connection can access stablecoins. This has significantly accelerated stablecoin adoption across global markets, especially in regions with weak or unstable financial infrastructure.

As digital commerce grows, stablecoins are becoming more important for moving value efficiently.

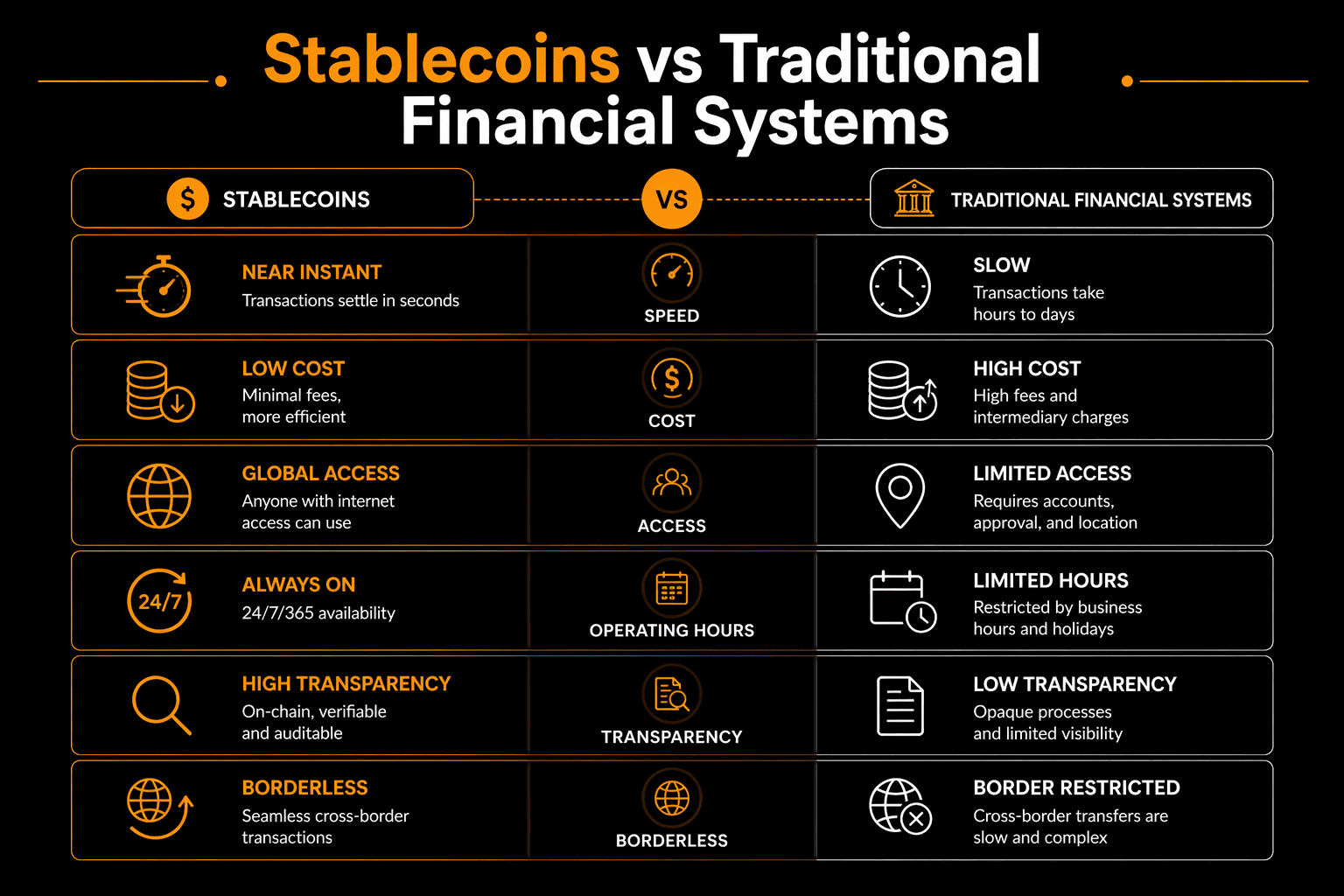

Stablecoins vs Traditional Financial Systems

Comparing stablecoins with traditional banking highlights why this transition is happening.

Traditional financial systems were designed for a world with national borders, limited connectivity and paper trails. They rely on clearing houses, correspondent banks and lagged settlement procedures.

Stablecoins are another matter. Transactions on a blockchain network are settled instantly, often in minutes or even seconds. Fees are usually more stable and cheaper. Access is global by default.

| Feature |

Stablecoins |

Traditional Banking |

| Speed |

Near instant |

One to three days |

| Cost |

Low |

High |

| Access |

Global |

Limited by geography |

These advantages are further enhanced when integrated with layer 2 scaling solutions like Polygon zkEVM that improve speed and reduce transaction costs.

This analogy explains the rising frequency of discussions about stablecoins vs traditional banking systems. Inherent flaws in stablecoins expose the inefficiencies that legacy systems can no longer hide.

Role of Stablecoins in Global Payments

One of the best uses of stablecoins is for cross-border payments.

For centuries, international money transfer has been a costly multi-step process with fees and delays. This process is greatly simplified by stablecoins. According to Forbes, research shows that stablecoin transfers typically cost less than $0.05, making them ideal for cross-border payments and remittances. Businesses handling high transaction volumes often integrate crypto wallet app development solutions to streamline global payment flows.

It is easy to see how stablecoins enable cross border payments. No matter where they are, stablecoins can be sent directly from person to person. Transactions are transparent, costs are low and settlement is fast.

It has changed international trade, global freelancing and remittances. Companies can pay their suppliers more quickly. People don’t need to depend on expensive banking rails to get money.

With the digitalization of global trade, stablecoins are increasingly becoming the preferred way of moving value around the world.

Stablecoins in DeFi and Web3 Ecosystems

Stablecoins have a big role in decentralized finance.

Stablecoins serve as the primary assets for lending, borrowing, trading, and providing liquidity in DeFi ecosystems and have liquidity provided for them in decentralized finance (DeFi). They offer a reliable unit of account in an otherwise volatile environment.

Most DeFi systems would not be usable by regular users without stablecoins. Stablecoins give you the ability to hedge risk, borrow and earn interest without the constant exposure to market volatility.

The role of stablecoins in Web3 ecosystem has a broader purpose, beyond their financial role. They are used in NFT marketplaces, gaming economies, creator platforms and decentralized applications where pricing consistency is key.

Stablecoins act as a core layer within decentralized applications powered by Web3 dApp development frameworks.

Enterprise Use Cases of Stablecoins

Businesses are no longer experimenting with stablecoins – they are actively integrating them into operations. They are actively integrating them into their operations. As enterprises look to implement secure and compliant stablecoin systems, many are turning to professional stablecoin development solutions to build customized payment, treasury, and settlement infrastructure.

Stablecoins for enterprise payment solutions are used to manage treasury operations, pay worldwide teams, settle foreign invoices, and speed up supplier payments. Advanced organizations also combine stablecoins with AI-powered financial analytics solutions to optimize treasury management and forecasting.

Businesses that run abroad want predictability and speed. That means companies can send money via stablecoins without having to wait for bank settlement cycles or pay large foreign exchange fees. Technology studios such as Chicmic Studios play a key role in helping businesses build and integrate blockchain-based payment and financial solutions at scale.

They also add transparency. Blockchain based transactions make the audit and reconciliation more efficient which is very helpful for the big businesses.

Stablecoins are also closely connected with real-world asset digitization, enabling seamless value transfer across tokenized ecosystems.

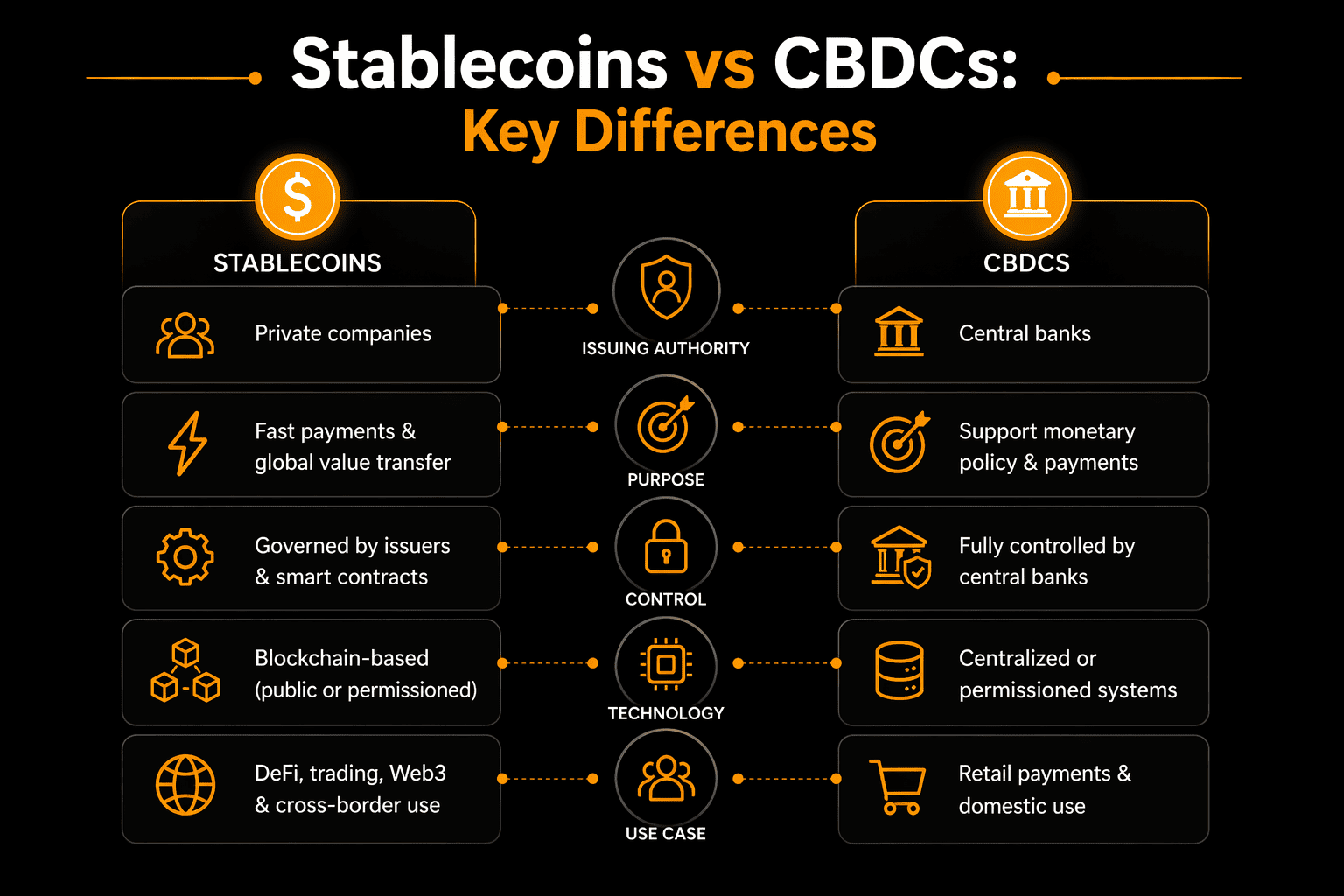

Stablecoins vs CBDCs: Key Differences

Central bank digital currencies and stablecoins are often used interchangeably, but they serve different purposes. Stablecoins are market-driven tools designed for fast, global digital payments and interaction with modern financial systems. CBDCs , on the other hand, are government-issued currencies that emphasize monetary control and domestic payment systems . Both are likely to play different roles in the emerging digital finance ecosystem rather than competing head-to-head.

The simple comparison table below highlights the key differences between central bank digital currencies and stablecoins in terms of use, control and structure.

| Aspect |

Stablecoins |

Central Bank Digital Currencies (CBDCs) |

| Issuing authority |

Issued by private companies or organizations |

Issued and controlled by central banks |

| Primary purpose |

Enable fast digital payments and global value transfer |

Support national payment systems and monetary policy |

| Geographic scope |

Operate globally across borders |

Mainly designed for domestic use |

| Technology base |

Built on public or permissioned blockchain networks |

Usually built on centralized or controlled digital systems |

| Use in digital markets |

Widely used in digital markets, DeFi platforms, and Web3 ecosystems |

Limited or experimental use in digital markets |

| Cross border capability |

Designed for seamless cross border transactions |

Cross border use is still limited or in early stages |

| Level of control |

Governed by issuers and smart contract rules |

Fully controlled by central banks |

| Role in the financial system |

Acts as a bridge between traditional finance and digital ecosystems |

Acts as a digital extension of existing fiat currency |

| Coexistence potential |

Can complement existing financial systems and CBDCs |

Expected to coexist with private digital currencies |

Risks and Challenges of Stablecoins

Despite the advantages of stablecoins, they have serious disadvantages.

Regulatory uncertainty is still a big issue. Governments are still working out how stablecoins will fit into existing financial regulations. Reserve transparency is important because trust relies on the belief that stablecoins are fully backed.

Custody and security threats must also be addressed. That’s why the significance of stablecoin regulation and compliance trends is increasing.

Stablecoins are gaining institutional credibility and legitimacy, thanks to clear mechanisms for consumer protection, licensing and audits.

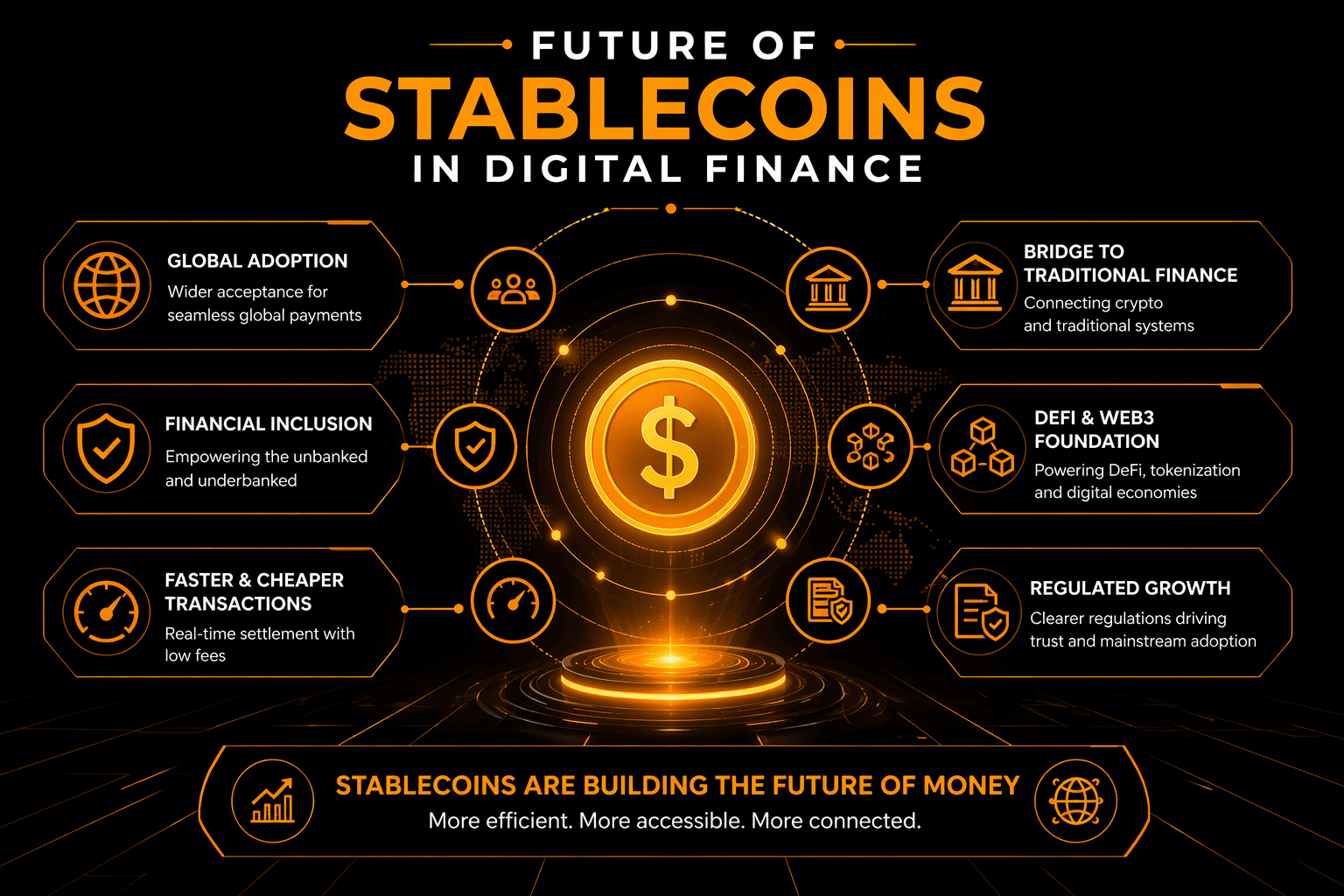

Future of Stablecoins in Digital Finance

The future of stablecoins in digital finance will become more closely integrated with traditional financial institutions.

Stablecoins are likely to be incorporated into enterprise applications, payment networks and banking platforms. They may not always be visible to users but they will power settlement in the background.

As international business use of stablecoins grows, emerging markets will continue to lead the way in adoption. With more interoperability, stablecoins will be more usable across many networks and platforms.

Stablecoins aren’t disrupting overnight, they’re slowly remaking finance from the ground up.

The future of stablecoin infrastructure is also being enhanced by AI development solutions for automation and predictive financial insights.

Conclusion

Stablecoins are no longer on the sidelines of finance. “They’re becoming critical infrastructure.” At ChicMic Studios, we closely track how stablecoins and Web3 technologies are reshaping global financial infrastructure for businesses and digital platforms.

They are addressing age-old problems of speed, cost and access in everything from global payments and DeFi platforms to enterprise finance and Web3 apps. Their power lies in their ability to combine digital efficiency with stability.

As acceptance grows and regulations evolve, stablecoins are doing more than just digital finance. They are becoming a core part of the financial system.

Turn stablecoins into a competitive advantage for your business.

Frequently Asked Questions

1. What are stablecoins in digital finance?

Stablecoins are digital currencies designed to maintain a stable value and are used for payments, settlements, and financial applications.

2. Why are stablecoins important for financial infrastructure?

They enable faster, cheaper, and more accessible financial transactions compared to traditional systems.

3. How do stablecoins support global payments?

They allow near instant cross border transfers with minimal fees and high transparency.

4. Are stablecoins better than traditional banking systems?

They outperform banks in speed and cost for many use cases but currently complement rather than replace them.

5. What industries use stablecoins?

Fintech, global trade, remittances, DeFi platforms, Web3 ecosystems, and enterprise finance use stablecoins.

6. What is the future of stablecoins in finance?

Stablecoins are expected to become deeply integrated into global financial infrastructure and digital payment systems.